WKU ranks among highest in nation in student loan default rates

November 6, 2014

WKU students are more likely to default on paying off student loans than students at University of Louisville or University of Kentucky.

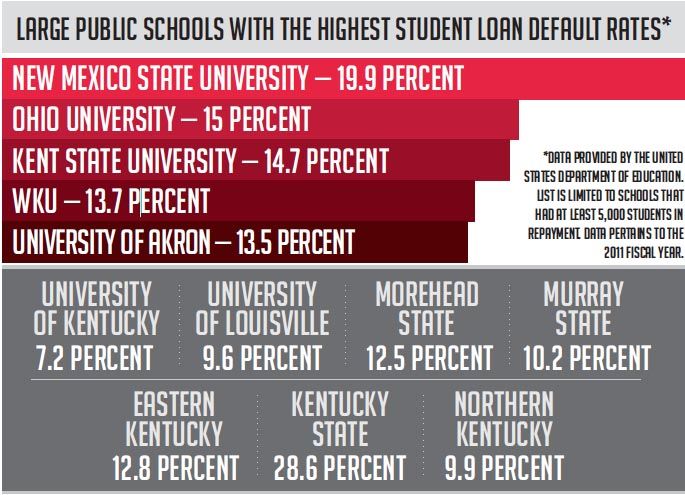

According to data released by the U.S. Department of Education in September, WKU’s three-year cohort default rate of student loans for the 2011 fiscal year is 13.7 percent with 5,237 students in repayment and 720 students in default. The percentage includes graduates and dropouts.

Cynthia Burnette, student financial assistance director, said WKU’s student loan default rate isn’t favorable.

“Our default rate is higher than we would like,” Burnette said. “We have a plan where we are putting more aggressive efforts in place to try to help those students who are in that repayment process.”

Burnette said students go into repayment six months after they graduate or are no longer considered a student.

According to the Department of Education, the nation’s overall default rate is 13.7 percent. However, Kentucky’s overall default rate is much higher at 17.5 percent, the fourth highest in the country.

According to the data, the University of Kentucky’s student loan default rate for the 2011 fiscal year is 7.2 percent with 4,273 students in repayment and 308 who have defaulted.

The University of Louisville’s rate is 9.6 percent with 4,171 students in repayment and 403 in default.

Andrew Head, WKU financial planning program director, said students typically default on loans due to a lack of employment options or entering career fields that do not earn them enough money to pay back loans. Some default students also may have a disability or long-term illness that causes them financial trouble.

Using data from the Department of Education, qz.com ranks WKU as No. 4 with the highest default rate in the nation for large public schools behind Kent State University at 14.7 percent, Ohio University at 15 percent and New Mexico State University with the largest at 19.9 percent. These percentages represent the fiscal 2011 three-year default rates for universities with at least 5,000 students in repayment.

“If you look at overall default rates we’re right at the middle,” Head said.

Head said he has seen the impact of those who have cumbersome student loans.

“I have had experience with students that have graduated from WKU with well over $100,000 in student loan debt and are going into careers that pay…25-to-$35,000 starting,” Head said. “It’s very difficult to make that kind of payment.”

He described the difficulty of paying off a student loan with the example of a $100,000 loan.

For a 10-year payment plan, Head calculated the initial payments would cost $1,151 a month, which is the bulk of take home pay for someone making $25,000 to $35,000 a year. If it were a 20-year scenario, the payment would cost $763 a month.

“A lot of people just really don’t know what the consequences are post-graduation as far as what these (loans) are going to cost on a monthly basis,” Head said.

Burnette said students are not always aware of when they are entering repayment options.

“There are options,” Burnette said. “There are multiple repayment plans. It’s not where there’s just one plan, and if you don’t fit in that plan then you’re subject to go into default. It’s not that way at all.”

The Student Financial Assistance office provides a variety of plans such as standard repayment plans and income-based plans.

“There needs to be considerably more candid discussion about job expectations associated with certain career choices and income expectations,” Head said. “There needs to be a very thoughtful discussion with students about the ramifications of borrowing these loans.”